Debunking common myths about embedded finance (EF)

Embedded Finance has emerged as a dynamic force in the rapidly evolving world of financial technology. However, certain misconceptions and myths have surfaced along with its growing popularity.

In this blog post, we take a closer look at six common myths surrounding embedded finance and uncover the truth behind them to help you better understand the vast potential and real impact of this innovative solution.

Embedded finance (EF): A $138 billion market outlook

In an era driven by financial technology innovations, embedded finance is emerging as a formidable force. According to a recent Forbes report, the estimated market value for embedded finance is projected to surpass a staggering $138 billion by 2026. This revelation showcases the immense growth potential and the transformative impact of embedding financial services into non-financial platforms.

However, some industries are still reluctant to make the leap to this innovative solution. Here are some of the most common myths about embedded finance:

Myth 1: It is only for big businesses

Fact: With advancements in technology and the rise of fintech startups, businesses of all sizes can leverage embedded finance solutions. It offers opportunities for small and medium-sized enterprises to enhance their customer experience, monetize their offerings, and drive growth.

Myth 2: It is just about payments

Fact: While payments are a key aspect of embedded finance, it goes beyond that. Embedded finance encompasses a wide range of financial services, including banking, lending, insurance, investing, and more. As mentioned previously, it involves integrating these services into non-financial platforms, providing comprehensive and seamless financial experiences for customers.

Myth 3: Implementing embedded finance is complex and costly

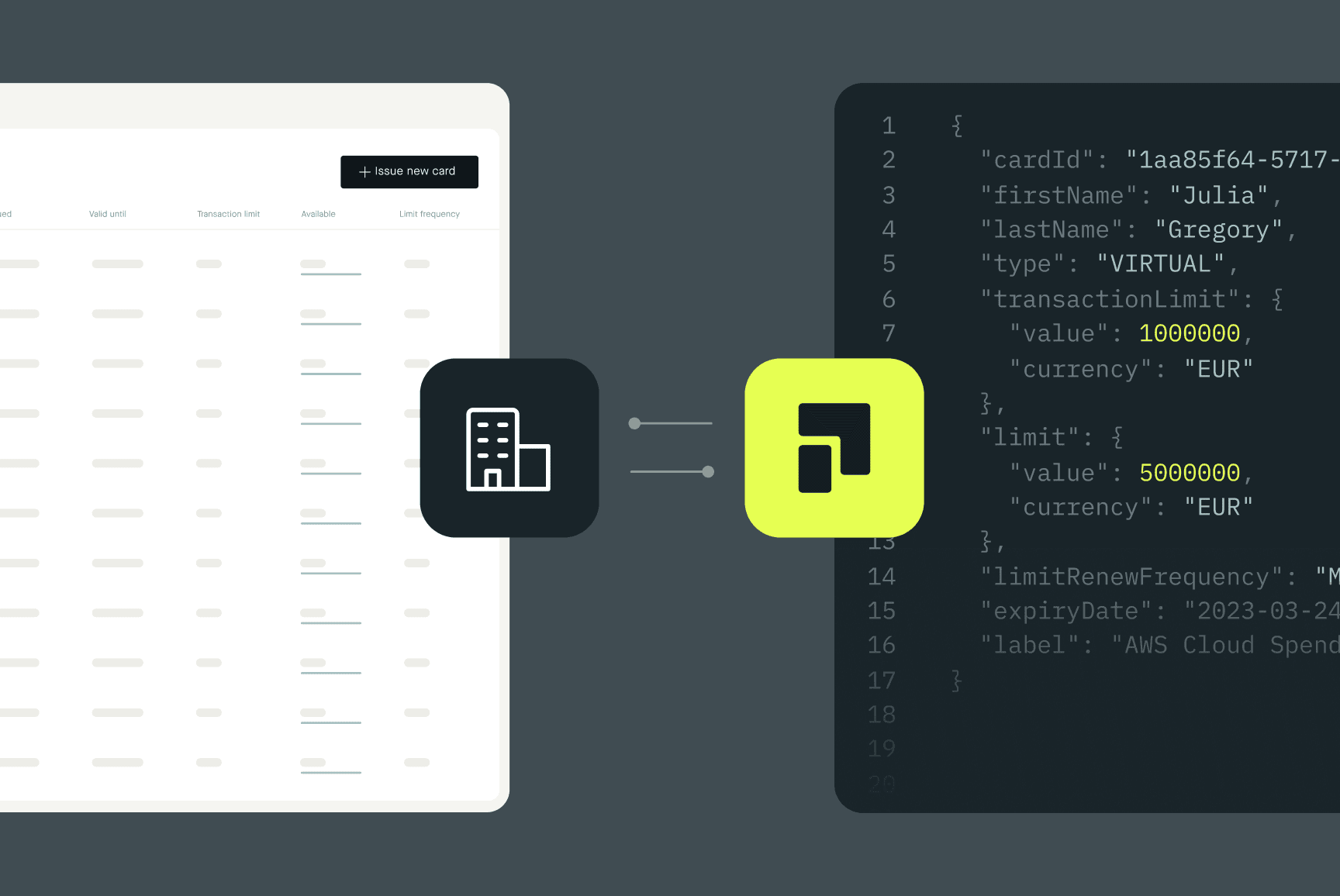

Fact: While integrating financial services can involve some complexities, advancements in APIs and partnerships with fintech companies, like Pliant, have made it easier to implement embedded finance solutions.

Pliant offers developer-friendly APIs and turnkey solutions, reducing implementation costs and time. This enables businesses to leverage embedded finance without significant upfront investments.

Myth 4: It replaces traditional banks

Fact: It doesn’t seek to replace traditional banks. Instead, it collaborates with financial institutions, leveraging their expertise and regulatory frameworks.

Actually, it often partners with banks, using their infrastructure to provide financial services to customers. It creates a win-win situation by enabling non-financial businesses to offer banking services while leveraging the stability and security of established banks.

Myth 5: It compromises security and compliance

Fact: Embedding financial services within platforms allows for stricter security measures and compliance adherence. EF platforms work closely with regulatory bodies and employ robust security protocols, ensuring data protection, fraud prevention, and compliance with industry regulations.

Myth 6: It leads to loss of control over customer relationships

Fact: When financial services are embedded within a platform, it actually strengthens customer relationships by providing a seamless experience. Businesses that offer embedded finance retain control over the user experience, branding, and customer interactions while leveraging financial services to enhance their value proposition.

Leverage embedded finance to the fullest

As you can see, embedded finance is not limited to large corporations.

What's more: While payments are a critical aspect, embedded finance encompasses a wide range of financial services. Thanks to advances in APIs and partnerships with fintech providers like Pliant, implementing embedded finance has become more accessible and cost-effective.

Despite the misconception of replacing traditional banks, embedded finance works with financial institutions, leveraging their expertise and regulatory frameworks.

EF also prioritizes security and compliance, working closely with regulators and implementing robust security. The important thing is that you never lose control of your customer relations, but rather enhance them through a seamless user experience.

💳 To learn more about how Pliant seamlessly complements embedded finance, click here.